Six Lies People Tell Themselves That Keep Them in Debt

There are liars everywhere — especially true when it comes to money.

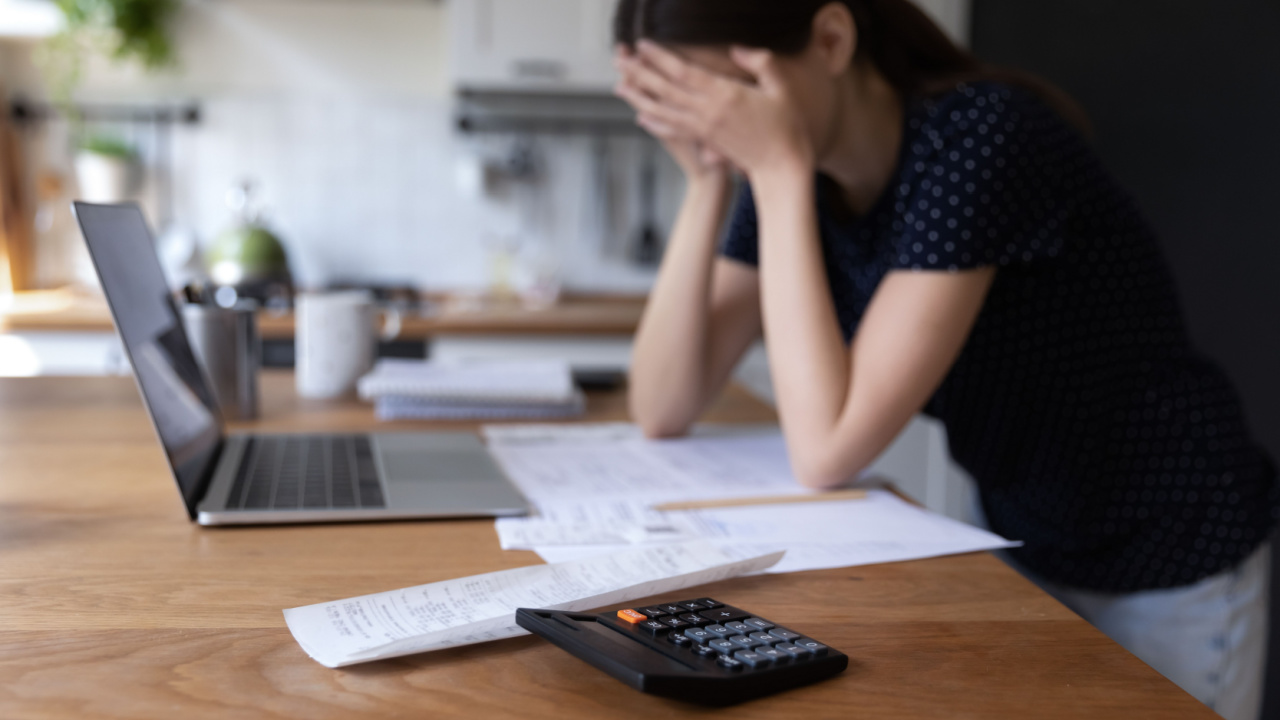

Sadly, debt has become an unfortunate companion for many. The path to financial freedom is often obstructed by the lies people tell themselves, unknowingly perpetuating a cycle of constant debt. The higher the interest, the worse the debt is. This is why credit card debt is considered the worst type of debt in existence.

It’s time to unveil the shackles and confront these falsehoods that keep individuals bound to the clutches of debt.

Five Lies That Keep People in Debt

Lie #1: “I deserve it”

Eliminate the word “deserve” from your vocabulary right now. The word “deserve” is very close to “entitled,” and those are words that keep people living stressful, unsuccessful lives.

Whether it’s a luxurious vacation, the latest gadget, or a high-end fashion item, the belief that one deserves instant gratification can lead to impulsive spending and mounting debt. The truth is, while treating oneself is important, it should be done within the bounds of financial reality. Overspending in the name of deserving something can pave the way to a debt-ridden future.

Instead, do this: Adopt a mindset of delayed gratification. Prioritize needs over wants and set realistic financial goals. Create a budget that allows for occasional treats without jeopardizing long-term financial well-being.

Lie #2: “I’ll start saving tomorrow”

Procrastination is a silent partner in the journey to debt. The longer you wait to pay off your debts, the more devastating they become.

Many individuals convince themselves that they will start saving tomorrow, perpetually delaying initiating a savings plan. Without a safety net, unexpected expenses can lead to borrowing and accumulating debt.

Instead, do this: Break the cycle of procrastination by setting specific and achievable savings goals. Create an emergency fund to cover unforeseen expenses, ensuring a financial buffer that prevents reliance on credit for emergencies.

Lie #3: “minimum payments are enough”

Credit cards often lull individuals into a false sense of security with minimum payments. People convince themselves that meeting the minimum payment requirements is sufficient to keep debt at bay. However, the reality is that minimum payments barely dent the principal amount, allowing interest to compound and debt to linger (and grow).

Instead, do this: Don’t just pay more than the minimum. Pay off the entire balance of your credit card every month, with no exceptions. If you cannot afford to pay off the entire balance, then you cannot afford to make those purchases. Nothing destroys financial health quite like high-interest debt.

Lie #4: “I can borrow my way out of debt”

Some individuals fall into the trap of taking out new loans to pay off existing debts, believing they can borrow their way out of financial trouble. This strategy often results in a vicious cycle, leaving individuals with a web of interconnected debts and mounting interest.

Instead, do this: Rather than accumulating more debt, develop a strategic debt repayment plan. Prioritize high-interest debts and work towards paying them off systematically. Seek financial advice if necessary to explore debt consolidation options or negotiate with creditors for more favorable terms.

Lie #5: “I’ll deal with it later”

Avoidance is a common coping mechanism when it comes to financial issues. People often tell themselves they’ll deal with their debt problems later, pushing crucial decisions down the road. However, delaying action only allows debts to grow, making the eventual resolution more challenging.

Instead, do this: Confront financial issues head-on. Assess the extent of the debt, create a realistic plan for repayment, and seek professional advice if needed. The sooner you address your financial challenges, the easier it is to implement effective solutions and prevent the escalation of debt.

Lie #6: “it’s only temporary”

Think debt is temporary, huh? Whether it’s a job loss, unexpected medical expenses, or other unforeseen circumstances, convincing yourself that the situation is short-lived can lead to complacency. This mindset often hinders proactive financial planning and can prolong the journey to debt recovery.

Instead, do this: Embrace the reality of the situation and create a long-term financial plan. Build an emergency fund to weather unexpected storms and establish a sustainable budget that accommodates both regular expenses and debt repayment.

In conclusion, breaking free from the chains of debt requires a commitment to honesty and proactive financial management.

By recognizing and dispelling the lies that perpetuate indebtedness, individuals can pave the way toward a brighter financial future. Adopting a mindset of financial responsibility, saving diligently, making strategic debt repayments, and facing financial challenges head-on are essential steps toward financial freedom.

It’s time to rewrite the narrative, dispel the lies, and reclaim control over your financial health.